Forum

Warto wiedzieć

Twoje Forum

-

Reko od BM Santander 20.30 zł

[217.96.215.*]

Wydane dziś i komentarz niestety po Angielsku

Ale myślę zenie sprawi problemów

Equity story. We maintain Outperform rating for Torpol. The decision concerning the retention of record high 2022 profits came in disappointing, as we expected the company to maintain its dividend policy. Nevertheless, we still believe in an appealing equity story for Topol. First, the launch of KPO pre-financing funds (EU Recovery fund) has just materialised, which – as we see it – opened room for signing new large-size contracts. We also cannot exclude that CPK would potentially look for a 100% ownership holding (purchase of 50%+ stake requires announcement of a call tender offer) at the end of the day. Launch of pre-financing of KPO funds finally materialized. The bridge financing of KPO fund has been finally launched. PKP PLK has recently signed two large size contracts with Torpol and Budimex thanks to the implementation of the pre-financing mechanism. We expect Torpol to potentially sign new deals in the short-to-mid run based on PKP PLK’s declaration to sign a total of 10 contracts with contractors worth PLN4bn by the end of the year. Backlog gradually raised. Tiny backlog is no longer a risk factor for Torpol, we think. The recent signing of PLN500mn+ railway contract lifted Torpol’s backlog to c. PLN1.6bn based on our estimates, which materially improved the visibility of 2024E-25E sales/profits, we think. We also expect Torpol to continue backlog growth over 2023-24E, as we expect PKP PLK to continue contracts distribution. Financial forecasts unaltered. We significantly increase 2023E forecasts as we upped gross margin estimate and financial income (thanks to high net cash). We forecast, though, 2023E-24E profits at a level significantly below 2022 level, due to extraordinary high 2022 earnings/margins. We also expect 2023E negative operating CF due to cash consuming contracts execution. Still, we expect CF recovery as of 2024E-25E. We estimate terminal gross margin at the level 6%, which implies net profit forecast at PLN40mn+. Risks. (1) Any delays in the supply of contracts from PKP PLK/CPK, (2) Any higher than expected NWC utilisation over 2023-24E represents the key downside risk to our CF estimates and valuation of Torpol. Valuation. We decrease our Target Price to PLN20.3 from PLN22.7 due to changes in financial forecasts and keep the Outperform ratingOdpowiedz Zgłoś do moderatora 2 2- Re: Reko od BM Santander 20.30 zł [89.66.246.*]

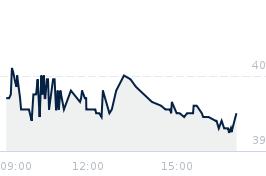

działaj ...ale było pond 20 jest 15

trzeba szukać poziomu wsparcia, ale póki co szykuje się sell in mayOdpowiedz Zgłoś do moderatora 1 3- Re: Reko od BM Santander 20.30 zł [188.33.248.*]

CPK po 21 zł kupujeOdpowiedz Zgłoś do moderatora 1 2- Re: Reko od BM Santander 20.30 zł [46.204.44.*]

Póki co nie ma espi więc nie wiadomokto kupuje ani kto sprzedajeOdpowiedz Zgłoś do moderatora 0 1- Re: Reko od BM Santander 20.30 zł [31.60.21.*]

To jest ważne, że są inwestorzy, którzy płacą ok 21 PLN za sztukę. Prawie połowę wszystkich akcji tak kupili. A Santander wycenia tylko na 20,30 PLN.Odpowiedz Zgłoś do moderatora 1 0- Re: Reko od BM Santander 20.30 zł [46.204.44.*]

Na pcc EXOL przy kursie 4zł kupowali pakiety po 5 i 7 zł. Potem spadł na 2,5 i do tej pory jest poniżej 3,5 a to było 2-3 lata temu...Odpowiedz Zgłoś do moderatora 0 0- Re: Reko od BM Santander 20.30 zł [83.26.168.*]

Ale na Pcc to raczej brali pakiety po 7zl żeby wywalać po 11zl, więc idąc dalej ta analogia powinien nam ładnie kurs pójść w goreOdpowiedz Zgłoś do moderatora 1 0- Re: Reko od BM Santander 20.30 zł [46.204.44.*]

Dopóki nie będzie marży porządnej, zamówień i dywidendy to zapomnijcie o kursie pow. 20 złOdpowiedz Zgłoś do moderatora 0 1- Re: Reko od BM Santander 20.30 zł [84.40.129.*]

Wszystko się wyjaśni kiedy ruszą pierwsze prace budowlane pod CPK.

Czekać Lipiec SierpieńOdpowiedz Zgłoś do moderatora 1 0- Re: Reko od BM Santander 20.30 zł [188.146.204.*]

Tu się już nic nie wydarzy a przynajmniej nic dobrego w perspektywie najblizszych miesięcy.Można sie pocieszac klepać po pleckach pisać kocopoły o mitycznym kupującym powyzej 20 który wie co robi a prawda jest taka że ta spółka z perły przerodziła się w zwykłego giełdowego trupa a poziom obecnej stabilizacji to wszystko na co ją będzie staćOdpowiedz Zgłoś do moderatora 0 1- Re: Reko od BM Santander 20.30 zł [188.147.4.*]

W zasadzie zgadzam się z tym choć nadzieja umiera ostatnia, na tym cmentarzu perły w koronie może coś jeszcze być wesołego np. akwizycja Pytań jest wiele co to to będze teraz Torpol czy Podtor .PiS to szambo totalne to co wyrabia się z biznesem w tym kraju w głowie się nie mieści , zero szacunku dla człowieka, prawa i jakichkolwiek zasad i praw własności. Rynek kapitałowy to podstawa rozwoju gospodarki, a za udostępnione środki trzeba płacić dywidendy przy takiej inflacji koniec kropka.- Kurs Euro

- Kurs dolar

- Kurs frank

- Kurs funt

- Wiron

- Przelicznik walut

- Kantor internetowy

- Kalkulator wynagrodzeń

- Umowa zlecenie

- Kredyt na mieszkanie

- Kredyt na samochód

- Kalkulator kredytowy

- Revolut

- Winiety

- Jak grać na giełdzie?

- Jak wziąć kredyt hipoteczny?

- Rejestracja samochodu

- Jak rozwiązać umowę z Orange

- Koszty uzyskania przychodów

- Sesje elixir

- PB weekend

- RRSO co to jest?

- Blogbank.pl

- Promocje bankowe

- Stopa procentowa

Przejdź do strony za 5 Przejdź do strony »Czy wiesz, że korzystasz z adblocka?

Reklamy nie są takie złeTo dzięki nim możemy udostępniać

Ci nasze treści. - Re: Reko od BM Santander 20.30 zł [89.66.246.*]